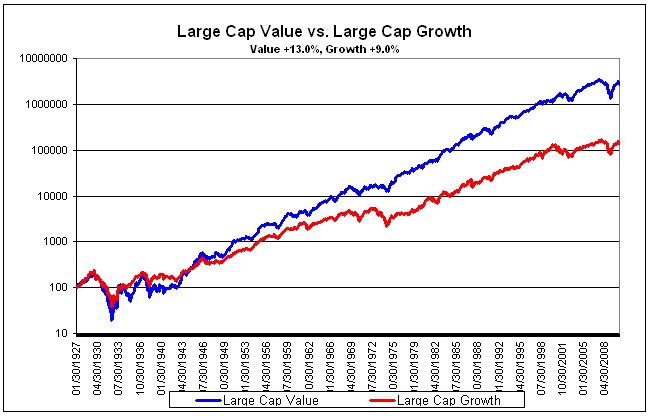

When you take the longest view of stock investing, a few patterns emerge, such as the importance of understanding value instead of investing according to an exciting “story.” Since this insight runs contrary to the way the Financial Infotainment Industrial Complex typically presents stock market investing, we need frequent reminders. Consider this your annual checkup.

By “value” I mean some sort of comparison between the price of purchasing shares, and the amount of annual corporate profits to which those shares entitle you. Common measurements for this value include the price to earning ratio (aka P/E ratio) and dividend yield, which is the ratio of dividends to stock price.

I recently read Jeremy Siegel’s The Future For Investors: Why The Tried And The True Triumph Over The Bold And The New, and found some nuggets in the book worth passing on, related to the theme of “value” investing versus “story” investing.

But first, a quick meta-point about the book’s subtitle. I agree with you that Siegel’s book sounds like the growling of a curmudgeonly old man, but I mean, you have heard of Charlie Munger and Warren Buffett, right? In other words, just because it sounds grumpy doesn’t mean it’s not also true. Also, the book isn’t new – it came out in 2005 – but again, refer to the subtitle to understand why newness doesn’t matter so much here.

Professor Siegel famously studies data on stock market returns to investors over the long term. For this book he tracked which large US companies provided the highest return, including reinvestment of dividends, over the previous fifty years. Did the best “story” stocks of 1957 triumph? Or were the best “value” stocks of 1957 better over 50 years? Would owning the entire universe of stocks have been the best approach, like what is now known as passive indexed investing?

I’ll jump to the punch line: it was the value stocks.

An investor picking the highflying technology companies of 1957, Siegel explains, would have experienced far lower investment returns than an investor picking relatively non-innovative consumer staples businesses.

The top four performers of the prior 50 years stand out as particularly boring consumer staples companies, not flashy technology companies. The winners were in the cheese, tobacco, oil, and sugar-water businesses, specifically National Dairy Products (later Kraft), RJ Reynolds, Standard Oil, and Coca-Cola.

In contrast, the “story” stocks, like the innovative engineering and technology companies of that era – GE, IBM, and AT&T – did fine, but far worse than the boring value companies.

In contrast, the “story” stocks, like the innovative engineering and technology companies of that era – GE, IBM, and AT&T – did fine, but far worse than the boring value companies.

Now, fifty years of stock market data doesn’t constitute Truth with a capital T when it comes to the future. But it’s a long enough period that we should keep it in mind.

And even if we don’t enthusiastically embrace “value” investing, the data is a nice reminder maybe of the dangers of paying too much attention to the “story” or optics of a stock, at the expense of value.

I really like another succinct way of saying all, by financial advisor David Hultstrom, who writes: “A good company or sector or country isn’t necessarily a good investment and a poor one isn’t necessarily a bad one. In fact the reverse is generally true.” For a contrarian like me, that line is a keeper.

A few other examples in this tradition stand out for me.

Warren Buffett famously bought a failing textile mill named Berkshire Hathaway, and eventually closed all of its mills. He bought a failing business in a failing industry, yet somehow acquired the roots of one of the world’s great fortunes.

Finance writer Morgan Housel also made this point dramatically a few years back in his presentation on cigarette company Altria Group Inc, which was the single greatest stock from 1900 to 2010. Smoking has declined steadily since 1981, the industry is not particularly innovative, and the regulatory environment is punishing. In other words, as a “story,” Altria is probably the worst stock you can possibly imagine.

But healthy dividends, reinvested at relatively low valuations, are what produced the extraordinary returns. In the fifty years from 1968 to 2017, an investment in the tobacco company grew by more than 20 percent per year, including reinvestment of dividends. Having said nice things about the stock, I do want to put in the obligatory statement for the kids: smoking isn’t cool.

The point is not really to seek to buy failures or failing businesses, but rather that the price at which you buy an investment, relative to its earnings – that famous P/E ratio – is more important than almost anything else about a company. You should try to remain undistracted by its “disruptive technology” or “innovative designs” or “rock-star management” or any other thing that tends to juice stock prices. So the tried and true advice is to mostly ignore the story, and look at whether the company generates actual profits on a regular basis. Yes, I embrace my inner curmudgeon, and so should you!

Finally, a disclosure note paired with pertinent advice: I own no individual stocks. I only invest in public markets through low-cost index funds and frankly you should do that too.

Finally, a disclosure note paired with pertinent advice: I own no individual stocks. I only invest in public markets through low-cost index funds and frankly you should do that too.

And given that, it is parenthetically interesting to me – and maybe to you – how much better Siegel found owning those consumer staple “value stocks” was to owning the entire S&P500 Index in 1957. I’m not changing my approach – for a variety of good reasons – but I’m just pointing out when a very good researcher’s data doesn’t back my advice or investment style.

A version of this post ran in the San Antonio Express News and the Houston Chronicle.

Please see related post:

Book Review: Stocks For The Long Run by Jeremy Siegel

Post read (931) times.